The individual or the enterprises today have an enormous digital footprint. However, this digital footprint is in form of data spread in silos across the entire economic system right from banks, AMCs, brokers, insurance companies, telecom companies, etc. Further, there is no single touchpoint from where this data is easily accessible or manageable. Therefore, the applicants requiring financial products have to collate, collect and share their documents either physically or in some cases digitally.

In terms of companies, some can generate data partly through securing permissions and accessing data whereas others have to go through the arduous task of generating and collecting data physically. Even after the hassles undertaken by the FIs, such benefactor entities cannot use the data to generate additional revenues.

All in all, no existing framework allows users to access data from one single touchpoint and entities to access user data even with the user’s explicit consent. Therefore, even we are ‘data rich’, we cannot leverage the data for making ourselves ‘economically rich’.

To solve this problem in March 2016, RBI approved a class of NBFCs called the Account Aggregator (AA) and created a framework called the Account Aggregation.

Similarly, before India, Europe started the initiative of Open Banking which is similar to account aggregation in India by the adoption of the Payment Services Directive (PSD2). The purpose of PSD2 was to increase competition and participation across Europe in the payments industry from banks and non-banks. It intended to provide a level playing field by harmonizing consumer protection and the rights and obligations for payment providers and users by increasing the usage and development of digital payments/banking through open banking. In August 2016, United Kingdom Competition and Markets Authority passed a ruling that required the bigger banks in the UK to provide transaction-level data to licensed startups. As of January 2020, this led to the adoption by 202 regulated financial service providers who enrolled for Open Banking.

On similar lines, many other countries adopted open banking initiatives. Australia launched an open banking project as a part of its Consumer Data Rights. In Nigeria, a coterie of bankers got together for the Open Banking Nigeria initiative to drive the adoption of common API standards.

What is an Account Aggregator?

AA is a consent manager to manage the permissions for sharing of financial data whereas Account aggregation is the framework whereby data from one or several accounts (banks, NBFCs, Mutual Funds, etc) of an individual’s financial accounts are stored at one place. An account aggregator acts as a conduit providing data to FIU or a customer from a FIP based on the consent provided by the owner of the data.

Before going deep into AA, let us understand the participants and their role in the AA framework.

A FIP acronym for Financial Information Provider is a data fiduciary which holds data of the individuals or enterprises, think Banks, NBFCs, AMCs, Insurance Companies, etc. Further, A FIU is an acronym for Financial Information Users, which consumes the end data received from FIP to provide financial products to the end customer. However, in some situations, Banks play a double role – both as a FIP (Home Bank) and an FIU (Lender). For instance, a Bank wants to access a borrower’s data to determine her creditworthiness for a loan that exists with a bank that has the savings account of the borrower.

It is also pertinent to know that institutions regulated and by regulators like the RBI, SEBI, IRDAI, Pension Fund Regulatory and Development Authority (PFRDA) can become an FIU and/or FIP.

Source: sahamati.org.in

The data flowing from FIP to FIU is encrypted and it can be only be accessed and processed by FIU to whom explicit consent has been provided by the data owner. Further, as an AA is blind to data, the potential misuse and leakage of data are also prevented.

Incentives for the participants & the impact on the Eco-system

A) FIUs – Use Cases

There are several use cases that we believe will be exploited by the FIUs through the AA framework by the innovation of new products as and when the financial services keep on developing. However, we have listed some of the very common use cases below:

1. Lending

Assessing the creditworthiness of a customer has been one of the painstaking tasks for lending platforms in India. Other than the assessment of creditworthiness, banks and NBFCs will be able to increase the velocity of secured lending in the following manner:

- Reducing risk by de-risking their loan books and reduce their NPAs.

- Reducing of time taken to process a loan and reduce loan processing costs.

- Offering personalized and customized loans to the customers.

- Monitoring loan post disbursement to intervene in case of any red-flags.

With the introduction of the account aggregation, financial institutions would be able to start lending based on the cash flow generating ability of 8% of the MSME (who do not have access to formal credit) rather than lending them based on an asset.

2. Wealth Management

Source: sahamati.org.in

AA framework would not only facilitate the provision of net-worth, savings details, and other investments, but it also provides hints on the true risk aversion of the investor. Generally, wealth managers have assessed the risk appetite of the investor by simply asking about his risk profile. However, with AA, individual behavior could also be observed, thereby giving insights on true risk potential. This would enable the wealth managers to further prepare a customized portfolio for the investor.

With the advent of AA, wealth managers can focus on securing new clients as the advanced processes along with a simpler data collection process would now help them in managing their regular day-to-day operations.

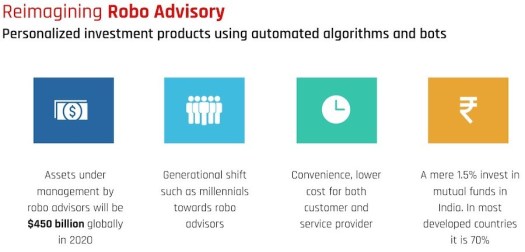

3. Robo-Advisory

In the current times, numerous millennials prefer investing through robo-advisory applications. However, the results of a robo-advisor depend on the algorithms, which have to be constantly updated. Therefore, with the advent of AA, where applications have real-time access to the financial data of individuals, robo-advisory applications can improve the quality of their decisions. However, to access the data, these robo-advisors would have to be registered and regulated by RBI, SEBI, IRDAI. Ergo, new aged fintech companies not registered with any of these laws would not be able to take the advantage of the AA, whereas large conglomerates having the financial might along with their multi-fold businesses would able to take advantage by creating a robo advisory platform.

Source: sahamati.org.in

Source: sahamati.org.in

4. Change in the user journeys for Financial Services customers

With the advent of AA, basic customer data like the personal details and bank account details will be readily available to the financial service providers. Following benefits would be readily available to the financial institutions:

- Prevention of customer drop-off from the various touch-points during the customer journey and reduced the KYC procedures for customers would also ensure increased convenience. Ergo, this would result in higher conversion rate for customers boosting revenue for financial institutions.

- Significantly reduce the chances of fraud, given the credible sources of the data.

B) FIP

The incentive for FIU is clear but why would a FIP share its valuable data? The answer lies in the principle of reciprocity. In case a financial institution does not share data, it will not be allowed to use or access data. Therefore, the incentive for a FIP is to have access to the data shared by FIU.

C) AA

The revenue model for an AA would be based on the level of differentiation and ease it can create for the FIU. Further, an AA would charge only charge FIU and the end customer for the provision of consent services. It is not allowed to FIP as this would hinder the progress of the Account aggregation framework.

D) Customers

From the customers’ perspective, they would not be required to run around with documents to procure loans, access to financial products, etc. This would, therefore, expedite the overall KYC, customer onboarding process, improve the overall customer experience for customers. the entire process is developed to ensure complete data blindness and customers are assured of complete data privacy.

Challenges in the AA Framework

While the AA aims to solve deeper problems like financial inclusion in India, there is also an impending challenge of data security posed by the AA. The unauthorized access by hackers may make the process gullible to fraud and unscrupulous transactions. Further, a single point of data aggregation makes the entire process vulnerable due to the sheer size and volume of public data available.

Another problem that is overcome is that the architecture of the AA system is primarily based on data sharing through technology with explicit consent. Ergo, aspects like API implementations, privacy frameworks, UI / UX design, cybersecurity, data warehouses would require significant IT capabilities for the FIU, FIP, and the AA. While the larger financial institutions may be affording such systems, the relatively smaller organizations may find it difficult and would prefer outsourcing such functions. To overcome such situations, it is pertinent to be assisted by a technology service provider. Pirimid Fintech being a Sahamati impaneled certified technology service provider can help.

How can Pirimid Fintech help?

Pirimid Fintech can provide expert consulting & end-to-end development for AA implementation. It can help the participants of the AA start-up ecosystem in the following way:

For FIPs: The plug & play modules developed by Pirimid connect securely with core banking systems to help you get started without any additional development efforts.

For FIUs: Pirimid also has its pre-listed modules for the adoption of the AA framework which can ensure that the FIUs start their AA journey in a hassle-free manner.

For further details refer to https://pirimidtech.com/solutions/account-aggregation/

This is a guest post by Yash Surana, who is a CA and an MBA (Finance) from SPJIMR, Mumbai, and loves writing about finance, strategy, startups & Personal Finance.